|

If your credit has fallen due to unforeseen circumstances, you need not to worry. Having a low credit score can feel like you have dropped into a rabbit hole you cannot climb out of. Financial instability can be life-altering and very stressful. If you fall into such a situation, all is not lost. SmartCredit has innovative tools you need to not only bounce back but bounce back strong. One of our tools within our platform is ScoreBuilder*. ScoreBuilder is a unique platform that gives you a 120-day plan to help build yourself a better score. This personalized plan is catered to your specific needs and situation. It will help you understand what is hurting you, what is helping you and will guide you through an easy step by step process on how to increase your score. Additionally, ScoreBuilder will let you know what actions to take on your account. You can also use ScoreBuilder to view the negative accounts weighing down your score and what actions to take to fix them. 120 Days to Better CreditIf someone stopped you on the street and told you that you could have better credit in 120 days, would you believe them? What if they had proof and case studies to show you that with a simple plan that’s easy to follow, you have the opportunity to increase your score? Starting Score, Current Score & Goal ScoreRather than guessing what score you’ll get by following our plan, you’ll be able to log in and see your starting score, current score, and goal score. The easy step by step guide walks you through all the items on your credit report that are helping your score, hurting your score, and what actions to take to get closer to your goal score. Action CategoriesWithin ScoreBuilder, our goal is to teach you how to take action on your own. You’ll understand how errors, small debts, and the risk of identity theft stand in the way of your goal score. By following a few simple steps like removing mistakes from your credit report or wiping out old or small debts, you’ll get closer toward your goal score. These categories include: Fix credit report errors, get goodwill corrections, pay off or negotiate small debts, and remove identity theft. Within the action section, you’ll also be able to monitor your action history. Next Steps

Since you are likely dealing with multiple creditors, how they respond could vary. In many cases, you’ll receive a response via an alert from us. Other times, a creditor may update your report, which will then be picked up by the credit monitoring services causing an alert again on our end. Less commonly, a creditor may contact you directly with a question or to inform you that your file has been updated. This may be done in writing or via telephone. In rare cases, a creditor may not respond at all. Additional Things to DoCheck your ScoreBuilder monthly to assess your progress and, if necessary, take new actions to boost your score. In the meantime, use the other features of your membership to control your money and credit, including ScoreMaster

*Please note that active membership is required for complete Action results. This feature unlocks if you have negative credit data. The post What Is ScoreBuilder? appeared first on SmartCredit Blog. from https://blog.smartcredit.com/2020/07/10/what-is-scorebuilder/

0 Comments

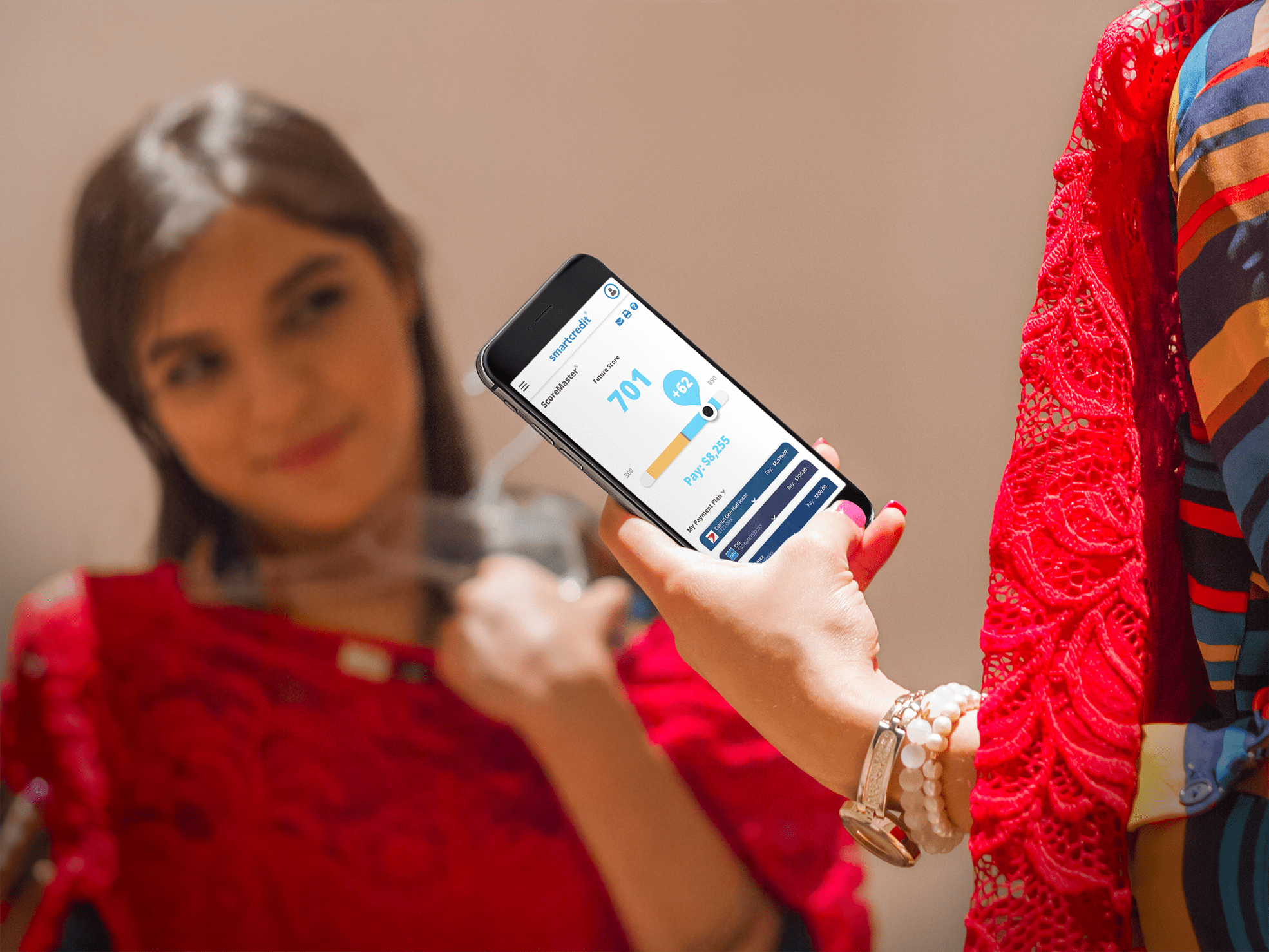

Has your credit ever gotten to an all-time low, and you didn’t know what to do? Are you trying to reach your dream credit score, but you’re not sure how to get there? With ScoreMaster, you can be the master of your credit score. Use ScoreMaster before you apply for credit, make payments, or spend money. Below we dive into a common question: What is ScoreMaster? ScoreMaster is a tool within the SmartCredit platform. SmartCredit offers an interactive credit report that’s easier to read and understand than a traditional credit report. Rather than making you scroll through pages of account history, the Smart Credit Report lets you flip through your credit report information piece by piece as if you were turning the pages of a book. SmartCredit is known for its gamification of credit scores with its ScoreBuilder, ScoreTracker, and ScoreMaster tools within the platform. If you want the ultimate control over your future credit score, ScoreMaster is the tool within SmartCredit for you. Know the best time to apply for credit, how much your payments should be for maximum credit score boost, and the best way to spend your money with minimal credit score impact. Score FluctuationsWith ScoreMaster, you can see how your score can fluctuate up and down rapidly. Use the dial within ScoreMaster to see how your credit score moves based upon your payments or spending on your revolving accounts (mainly credit cards). These accounts are the most volatile portion of your score and can change rapidly because banks and creditors update your report monthly to reflect your payments and your spending. Future ScoreWant to see what it’ll take to get to your dream score? You can move the ScoreMaster dial to the right of your current score to see how your credit score may increase when you make payments to any of your revolving accounts. It’s common to see an increase within 15 to 45 days after your payments post, when you reach the target statement balance and when everything else on your credit stays the same or remains normal. Curious to what will lower your score? Move the dial to the left to see how spending on your revolving accounts could lower your score. It’s common to see a decrease in 15 to 45 days after spending or missing a payment. To increase your score, make sure to quickly pay the amounts you spend on your revolving account ideally within ten days, but at minimum before your monthly statement balance is generated by your credit or bank provider. By paying before it’s reported, you can help avoid a decrease in your score. This is incredibly important before applying for new credit. TimingTiming can be everything, especially when it comes to your credit. One of the most important factors for getting approved and getting the best deal is timing. Rather than getting denied and a negative mark from a hard inquiry, you can monitor your score and see if you’ve taken all the actions you need before you apply. With ScoreMaster, you will know the optimum time to apply for a credit card, auto loan, mortgage, or other forms of credit. PaymentsNot only can making payments on time help your score, paying the right amount at the right time can make all the difference. With ScoreMaster, you’ll see how your payments can increase your credit score, and you’ll know exactly how much to pay and when to help maintain or improve your credit score.

SpendingSee how your spending can lower your credit score. Balance the spending between your accounts and know the optimum time to repay. MonitoringWe will actively monitor your credit cards and credit report to alert you of changes and detect fraud as your credit score changes. Ready to become the master of your credit score with ScoreMaster? View our Membership Options. *Legal Disclaimer – ScoreMaster is a patent-pending educational feature simulating credit utilization’s effect on credit scores via payments or spending. Your results may vary and are not guaranteed. The post What Is ScoreMaster? appeared first on SmartCredit Blog. from https://blog.smartcredit.com/2020/07/09/what-is-scoremaster/

The economic crises we are facing is unprecedented. It’s challenging to ascertain what the future holds with over 20 million job losses in the United States. People are anxious, stressed out, and worried about their future. Although protecting your credit and identity should always be top of mind, it is even more critical to protect your credit & identity during COVID-19. The last thing any of us needs are issues with our credit score, or worse, our identity. As we all know, the COVID crisis is not localized. Every corner of the earth is experiencing its effects. According to reports from Global News, the coronavirus has taken a significant toll in Italy. Over 41% of those polled said they are worried about their financial future. Now that the U.S. has exceeded those cases, the number of Americans that are worried about their financial future is on the rise. PROTECT YOUR CREDIT & IDENTITY DURING COVIDWATCH FOR PHISHING SCAMSSome great programs are currently available to help provide financial relief to both individuals and businesses. However, scammers are playing on people’s fears and anxieties around COVID-19. As local government assistance continues to come forward, it’s essential to know that government agencies such as the IRS, Medicare, Medicaid, U.S. Department of Health and Human Services, and Social Security rarely call consumers directly. They also less commonly ask for a fee of any kind over the phone. Additionally, there are fake government websites that are lurking around the internet. Keep an eye out for a lock at the top left corner of the URL and if the domain is a .gov. If you see these, the website is likely safe. Think you may have ended up on an unsafe site? It’ll be important to monitor your identity online. You can also take additional precautions by investing in Identity Fraud Insurance*, which comes free with your SmartCredit membership.

PLAN AHEADWhen it comes to COVID-19, the number of active cases is continually changing. Our experts have an idea but no clear roadmap to how the next 3-6 months will be, causing an air of uncertainty around the future. Because of this, it is vital to create punctilious budgets. If you foresee an issue with your future finances, consider tightening your budget to ensure that you will have enough funds to cover your future expenses. You can also plan your spending with ScoreMaster®. ScoreMaster allows you to know the optimum time to apply for a new credit card, auto loan, or mortgage, watch how spending and payments can lower or increase your score, and keep an eye out for credit card fraud.

CONTACT LENDERSIf you’re having trouble making payments, you might be able to temporarily lower your payments, defer your debts or mortgage, or lower your interest rates. Since the COVID-19 pandemic started, many lenders have put policies into place to help their customers gain extra time to complete their payments. If you know that you won’t be able to pay a bill by its due date, reach out to your lender to find out about any available hardship options.

REPORT LOST CARDS IMMEDIATELYWith the easing of restrictions, you may soon be in a situation where you become absent-minded and forget your credit card. It has happened to us all, especially when you haven’t shopped for months. If such an unfortunate event occurs, there is no need to worry. Just call the credit card company and report it lost immediately. The sooner you report a card stolen, the less likely you’ll be hit with a future fraudulent transaction. PROTECT ONLINE & IN-STORE PURCHASESThere are a few precautions you can take when sliding your credit cards for commercial transactions. Firstly, store your credit card in a secure location at all times. Be cognizant during the checkout line for transactions done at stores. As soon as you complete your purchase, double-check to see if you placed your card back. Only allow very secure payment portals to remember your credit card number. Examples of these include Google Pay, Apple Pay, and PayPal. A practice that would even keep your transactions more secure would be not to use the “remember card number.” In our day and age, online purchases are unending. Before you consummate an online transaction, ensure that the website is secure and authentic. Make sure that the URL for the site is trustworthy. There must be an “s” at the end of the http for the web address. Also, make sure that you see a lock icon. If your credit card was placed in jeopardy, you can set spending alerts, and set daily transaction reports with the SmartCredit Money Manager. We are in a time of anxiety, stress, and uncertainty due to COVID-19. Take a step back and remain positive about the future. The future is in your hands, and you can take the steps necessary to keep it protected. If you have any additional questions about how to protect your credit & identity during COVID, please feel free to browse more information on our website and social media pages. The post 5 Ways to Protect Your Credit & Identity During COVID-19 appeared first on SmartCredit Blog. from https://blog.smartcredit.com/2020/07/08/5-ways-to-protect-your-credit-identity-during-covid/

The secret to unlocking many financial opportunities? Good credit. An excellent credit score means lower interest rates on car loans, credit cards, and mortgages. Many landlords and employers also check credit reports before they make a job offer or approve a rental application. Since credit is based on spending, it’s important to know the best age to start credit monitoring. The answer might surprise you.

Under 18How young is too young when it comes to building credit and credit monitoring? If you’re under 18, one of the more popular options for building credit is to be listed as an authorized user on a credit card (owner must be over 25). In many cases, issuers don’t set an age minimum for authorized users since they aren’t responsible for any of the bills. Authorized user status allows for the teenager to benefit from the good credit history the signee is building. However, being an authorized user does not have the same credit-building power as being the primary user of the account; but it’s a start. Thinking about signing someone on as an authorized user, but you’re not sure if the person is ready? You don’t have to give them a card until you feel he or she is ready for the responsibility. Simply being the authorized user on paper is enough to do the trick.

18+ With a Co-SignerIf you or your child is over 18 and looking to increase their credit score more than authorized usership can do, there are other opportunities. A popular way to build credit between the ages of 18-21 is through a car loan or having someone co-sign on a student loan. The CARD Act of 2009 requires everyone under the age of 21 to have a co-signer or demonstrate their ability to pay. Full-time students will likely need to rely on a co-signer if they do not have a stable full-time job. If the applicant is under 21 and is not a student and has a full-time job with stable income, a co-signer may not be required. Remember, co-signing for the borrower comes with risks (in comparison to adding someone on as an authorized user on a card). As a co-signer, you’ll be responsible for paying if the borrower doesn’t. Be sure that you’re comfortable with this possibility before moving forward with co-signing. Co-signing a loan, credit card, or student loan are also additional options to help build credit. If you don’t have someone that can add you on their card or co-sign on a loan, a starter card might be your best first step.

18+ Without a Co-SignerIf you don’t have someone that will add you on as an authorized user or be a co-signer for you, getting a Secured credit card may be your best first step. Secured cards require an upfront security deposit to open. Your deposit typically equals your initial credit limit. For example, if you have $500, you’ll use this as your security deposit, and it will get you a $500 credit limit. Keep in mind; this doesn’t work like adding money into a bank account. Once you load in the $500, it doesn’t mean you freely spend $500. You will need to make payments monthly like a regular card, and once you pay on time for the contract, you’ll get the deposit back. These cards are easier to qualify for but are imperative that you pay them on time. Once you have one, or any loan, you’ll want to start monitoring your credit score.

Make Payments On TimeOne of the most significant factors when it comes to your credit score is how frequently you pay your bills on time. If you’re bad at remembering to pay things on time, consider setting due date reminders on your phone. Terrible at alarms? Schedule automatic payments from your checking account each month. The second you get your first card or loan, your number one goal should be never to miss a bill payment. Bill payments don’t just include credit cards. Once you’re 18, if you go to the hospital or have any bill that isn’t paid on time, you’re at risk for being taken to collections. Having a collection on your credit report can hurt your score.

Don’t Spend More Than You Can AffordThis should go without saying. Only pay for what you need and what you can afford. One of the next most important factors for your credit score is how much of the available credit you’ve been given and how much you use it. Let’s say you’ve been given a credit limit of $1,000, and most months, you carry a balance of $900. This may hurt your credit score. To learn more about how spending can affect your credit, use our ScoreMaster tool. Credit cards are not used for buying things you can’t afford; they are there to give you a little extra time to pay for a big purchase. It will likely affect your score and cost money in interest when you take more than 30 days to pay it off.

Stay on Top of Your Credit ScoreMonitoring is just as important as building your credit. If you do a ton of work to build your score, you’ll want to make sure nothing is hurting all that hard work. Credit monitoring is one of the best ways to learn what will positively or negatively impact your scores. It also helps you catch inaccuracies or signs of identity theft sooner. You can check your credit report for free, take action, and more with a seven day free trial of SmartCredit. If you’re someone who is thinking about their financial future, it’s time to commit to building your credit. Building your credit at a young age will likely make it more possible for you to get things later on in life, such as an apartment, car, dream job, or premium credit card that comes with points and exclusive benefits. Additionally, a better score can save you thousands of dollars in interest. The post The Best Age to Start Credit Monitoring appeared first on SmartCredit Blog. from https://blog.smartcredit.com/2020/07/07/the-best-age-to-start-credit-monitoring-and-building-credit/

T’is the season of love, or is it? The summer months from May to August fall under the wedding season. Unfortunately, with the arrival of COVID-19 many couples are having to postpone their wedding indefinitely, or do smaller and more personal ceremonies. With the wedding season among us despite the pandemic, many are still wondering – how does getting married affect my credit score?

One Spouse has bad credit; one has good credit.Many people wonder, will anything happen to my credit immediately after exchanging my nuptials? Although rumors have it that you marry your spouse’s score, that’s not the case. Both you and your spouse will have distinct credit reports after you tie the knot together. Once the union happens, your spouse’s credit history will not appear on your credit report. Neither will your information show up on your spouse’s credit report. Life happens to all of us. You have that student loan bill that piles up, or you happen to have taken a loan for a medical bill. If it so happens that the one you love had some financial mishaps, you need not worry. Your spouse’s score won’t change yours and if your spouse has a low score, no one will be able to determine that by looking at your credit report. Another positive thing to note is that your credit report will not drop points if your spouse has a low score.

Will Changing Your Name Have an Effect on your Credit Score?Another popular belief is that a name change or name alteration could change their credit score. If one spouse changes their name and reports the name change to their credit card companies, the new name will come up as a name variation on that person’s credit report. There is a false notion that if a spouse changes their name, their past credit history is eradicated. This is not true. Credit reports are linked to a person’s social security number. Once a spouse changes their name, they will continue to have only one credit report with accounts under the old and new names and the score will not be affected.

When Can Your Spouse’s Credit Affect Yours?There are cases where your spouse’s credit can affect yours. When lenders make a decision for a joint account, they will look into the financial history of both parties. If your spouse or both of you have bad credit, there is a possibility that your application could be denied. If the application does get approved and one party has bad credit, you may get hit with high-interest rates. When a joint account is made, both parties become responsible for the payments. If there is negligence, both will be affected. The lender will come after both parties.

Is Debt Shared When Getting Married?The individual debts both parties acquired before marriage remain their responsibilities. After marriage, you will bring upon joint debts. In the United States, there are “community property” states. These include Louisiana, California, Texas, Arizona, Washington, Idaho, Nevada, Wisconsin, and Alaska. These states will consider both spouses responsible for all the debts and assets during the marriage. This includes other liabilities and debts that one spouse has, even if the other spouse does not know. The other states go under what is called “common law” rules. In this situation, spouses have the option to take on debts and own properties as individuals. They can also take on joint debts that will benefit both parties (including any children) as a family.

Helpful TipsWhen two people come together to start their life, finances will be an important factor. An imperative decision that needs to be made is that you and your partner should put all your financial records on the table. This includes savings, investments, salaries, real estate, and, most importantly, credit. Sit down and review your credit reports together. It’s best to get a better understanding of each other’s financial situation now rather than get confronted with a crazy surprise further down the road! The question, how does getting married affect my credit score will always be on one’s mind. It is crucial to make wise decisions as financial stress can affect a marriage. If the situation arises that you and your spouse have varying credit scores, you have to decide together how you want to handle credit-based applications. The post How Does Getting Married Affect My Credit? appeared first on SmartCredit Blog. from https://blog.smartcredit.com/2020/07/06/how-does-getting-married-affect-my-credit/

Identity theft is a method of stealing someone’s identity in which an individual generates or creates a fake identity, this generally can be defined as a means to gain his or her hands on resources or procure credit. The victim of identity theft can literally experience serious consequences if they could be held as responsible for the thief’s criminal activities. Identity theft can only arise in scenarios takes place when someone can use other person’s personal identification information. To prevent such adverse scenarios from occurring, we discuss 10 aspects of identity theft below, which, if borne well in mind, can help you be smarter and staying protected from becoming a victim of this misdemeanor! https://www.smartcredit.com/credit-report.htm 1. IDENTITY THEFT THROUGH CHECKOUT LINESIf an individual or salesperson asks to take your card and takes long time to deduct the amount from your card and for bill payment than there is surely something wrong. They could be scanning your card for a handheld device or skimming terminal for harvesting your personal information. Due to advancement in science and technology, they can even take the front and back picture of your card with a cell phone and can swipe out cards. You have to be really aware in this regard as you may not know that they have swapped your card, Click here. 2. UNWANTED EMAILSIf you receive any email that is irrelevant to you and requires you to provide any personal information, you should instantly report this as a spam. Financial Services Companies never send such emails. Do ensure to be extremely discreet when you give out your personal financial information because if they are obtained by ill-intentioned people, they may use it to carry out a range of illicit activities in your name, and it is you who will have to bear the possibly very serious consequences for them. 3. THEFT THROUGH ONLINE GAMESOnline games, where individuals sign up to establish accounts, are a virtual method for thieves to steal personal information. The core objective of such scammers is to secure critical personal identity information. Sometimes, thieves send false emails, hoping to glean the personal information which gamers are asked to provide to able to play computer games. It would be wise, therefore, to only login through a safe and secure website. 4. THEFT THROUGH MILITARY OR ARMY INTELLIGENCEMilitary men and women are frequently required to provide their personal information in various places. This makes them vulnerable and sometimes, even the prime targets for fraud. Identity thieves can also be creating a fake program and could be offering a new program for military members, but such offers are only found out to be a hoax when those entering their personal information. But the damage has already been done! 5. FRAUD THROUGH TELE MARKETING OR COLD CALLSThere is a huge possibility that one may get call from an organization or individual that could seem to be legitimate or could be calling for a profitable cause. However, such calls could be illegal or scams. If you ever find such cold callers or potential scammers, find their toll free or land line number and call them directly to verify. https://www.smartcredit.com/credit-report.htm 6. FALSE WIFI HOTSPOTSWhile public Wi-Fi hotspots are very convenient, they do pose as a potential risk in as far as identity theft is concerned. Hackers create these hotspots to try and exploit innocent people who may be attracted by a browsing opportunity. Once you sign into a suspicious Wi-Fi hotspot, the hackers can access you device and retrieve your personal information or even personal data including username, passwords and any other important data that you’ve used online. You need to be very cautious about public Wi-Fi hotspots and avoid them if possible. 7. SYNTHETIC OR ARTIFICIAL IDENTITY THEFTWithin this form of identity theft, the identity of the thief is fictitious and also quite confusing. Scammers in this strategy amalgamate stolen identity of an individual and mix it with other fake or genuine information of another individual. It is very difficult to detect such crimes. 8. MAIL REDIRECTSIf you are receiving less email than usual or calls related to products you never requested you might be a victim of mail redirect. These kinds of schemes normally take place when a thief uses your personal information to alter your address. They redirect your mail to an address of their choice, where they can obtain your personal information and establish new accounts. Make a habit of stopping any junk mail and any suspicious request as they come to keep yourself safe from these kinds of malicious acts. 9. FRAUD THROUGH CHILDREN MANIPULATIONOne of the ways through which identity theft has become quite common in today’s time is manipulation of children. The fact can’t be denied that children are attractive targets of manipulation for crooks and thieves as they can propel children through a wide variety of ways to achieve their motive. It is important that parents are always aware and monitor every activity of their children. The activities can be various. From checking utility bills to calls received from school teachers and other relevant people. Apart from that, if there is any hesitation regarding why a school teacher or anyone from the school administration needs confidential information regarding your child, you not hesitate in asking questions. 10. TECHNICAL PROWESS OF HACKERSThe fact can’t be denied that online hackers and fraudsters are expert at science and technologically and can adapt to the core requirements of these crucial things. It is even difficult for cyber security specialists to detect such frauds from occurring. According to a research by Avivah Litan of the technology firm Gartner Group, less than one in 500 identity crimes could lead to a potential arrest. That does mean that such criminals have been growing consistently and are not being caught due to their innovative strategies. Such cyber threats have evolved so quickly that police are unable to get hold of such criminals and hackers are creating new techniques year after year. The fact that such thieves are certainly creative does make it difficult to catch them. You can also check Smart Credit. Origina Source:https://blog.smartcredit.com/2016/03/02/10-things-know-identity-theft/ from https://smartcredit2.blogspot.com/2020/07/10-things-you-should-know-about.html

If your primary obstacle to home ownership concerns the down payment, you are not alone. For many potential homebuyers, coming up with a down payment of as much as 20 percent seems insurmountable. Do not despair – there is a bright spot. You might qualify for a zero down payment mortgage. How do you buy a house with no money down? There are several options. Federal Housing Administration LoansWhile the majority of FHA loans require a 3.5 percent down payment – still very low – under certain circumstances borrowers may qualify for zero down payment or a token payment of 100 dollars. Those circumstances involve a down payment gift. Such a gift may come from relatives, employers, non-profit organizations or government agencies. A friend may provide the gift as long as you can document a substantial personal history between you. The U.S. Department of Housing and Urban Development (HUD) oversees FHA mortgages. While lenders are private, FHA guarantees the mortgage. As long as your credit score is at least 580, you may qualify for a 3.5 percent down payment loan. As long as your credit score is a minimum of 500, you might receive an FHA loan if paying 10 percent down. Federal student loan or income tax delinquency disqualifies borrowers. VA LoansIf you are a current or former member of the U.S. armed forces, or the surviving spouse of a member, you might qualify for a VA loan with 100 percent financing. Many buyers do not have to pay Private Mortgage Insurance (PMI) even with a no down payment loan, and VA loans offer low interest rates. Closing costs are also reasonable. While the U.S. Department of Veterans Affairs guarantees the mortgage, it is financed by a private lender. Zero down mortgages are only available to applicants with good credit and sufficient income. Rural Housing LoansThe U.S. Department of Agriculture offers no down payment loans for very low-to moderate-income applicants in eligible rural areas. Those meeting the income and area criteria may apply for a rural housing loan. Yes, rural housing loans target rural areas, but many of these designations are in or near places usually considered suburban. The USDA defines very low income as less than 50 percent of the Area Median Income (AMI), while low-income is between 50 and 80 percent of the AMI. Moderate incomes are under 115 percent of the AMI. Maximum income guidelines are strict, so anyone making over 115 percent of the AMI will not qualify. In general, rural housing loans only apply to dwellings of less than 2,000 square feet. If a new manufactured home is on a permanent site and purchased from an approved dealer, it may qualify for this financing. Only those with a sufficient credit history may receive these loans, but there is another caveat: They cannot obtain credit elsewhere. An applicant with a minimum credit score of 640 should receive loan approval. For those applicants whose adjusted annual income is less than 60 percent of the AMI, these loans are structured for repayment over 33 to 38 years. Zero Down Payment Loans and Bad CreditNot everyone looking for a home loan possesses a stellar credit rating. Is it possible to purchase a house with no money down if your credit rating leaves something to be desired? That may depend on your future prospects. Some credit unions offer zero down payment mortgage loans to members, but applicants must meet eligibility standards. Pay your bills on time and use other methods, such as SmartCredit, to achieve your future credit score, and you might receive approval. Programs are available in some states for doctors just out of medical school. These newly minted professionals usually carry a great deal in medical school debt, often more than the price of the average home in an area. If you are a recent medical or dental school graduate, check out Doctor Loan Programs in your region. Contact SmartCreditSmartCredit allows you to control your future credit score. Our system helps consumers achieve their best, opening up a world of possibilities – including qualifying for zero or low down payment mortgages. For a small monthly fee, not only do you receive credit reports and scores with SmartCredit, but access to ScoreMaster, credit monitoring and $1 million in identity theft insurance protection* for the entire household. Contact us today and find out what SmartCredit can do for you. *Activation required References:

The post How to Buy a House With No Money Down appeared first on SmartCredit Blog. from https://blog.smartcredit.com/2020/07/06/how-to-buy-a-house-with-no-money-down/

Beyond starting your career and planning some epic adventures, your 20s are a prime time to cultivate smart financial habits. After all, what you do in your 20s lays the foundation for your financial health in the long run. With 62 percent of millennials living paycheck to paycheck, it’s crucial to consider how the choices you make now will influence your financial future. From eliminating your debt to figuring out how much you should save in your 20s, here are five personal finance tips to set you up for long-term success. 1. Establish a BudgetNo matter what your salary amounts to in your 20s, it’s important that you come up with a budget that will allow you to pay your bills and save. Without a budget in place, you may end up overspending on frivolous items, like too many Starbucks lattes or take-out deliveries. In fact, the average 25- to 34-year-old reported spending $2,008 per year at coffee shops and an average of $2,800 per year on restaurants, with millennials ordering out more often than other generations. While nobody is suggesting you stop drinking coffee or never order food, it’s smart to know when a good thing is becoming a bad habit. By charting out your daily expenses and recurring monthly payments, you’ll know exactly where your money is going, and thus where you might be able to cut costs. You’ll then be more equipped to consider your short-term and long-term savings goals, including saving for a down payment if you ever hope to own your own home. 2. Make a Debt Repayment PlanFrom student loans to credit cards, debt is a burden for most Americans, and young adults are no exception. Millennials carry an average of $27,900 in debt, not including mortgages, and Gen Z have an average debt of $14,700. To prevent your debt from growing due to interest and/or late payments, construct a debt repayment plan, which may include setting up automatic payments. You might also consider joining programs that can help lessen the burden, such as the Peace Corps or Americorps. 3. Start Saving for Your RetirementRetirement might seem far away now, but it creeps up quickly, and saving early will benefit you tremendously in the long run. The sooner you start funneling money into a 401(k) or other retirement account, the longer that money has to accumulate interest and grow into a sizable nest egg that will support you in your golden years. If your company offers a 401(k), don’t hesitate from participating by having your contribution automatically deducted from each paycheck before taxes. The general rule of thumb is to try and save between 10 to 15 percent of your income for retirement in your 20s. 4. Build a Rainy Day FundA rainy day fund is just another term for an emergency fund, or money you can access if you suddenly lose your job or run into some unexpected expense. With an estimated 61 percent of millennials having less than $500 tucked away for emergencies, it’s easy to see how credit card debt can accumulate quickly when there’s no other choice to cover unforeseen costs. The standard advice is to put away three to six months’ worth of essential living expenses and take an oath not to touch the money unless you absolutely have to. 5. Improve Your Credit Score with the SmartCredit SystemHaving a healthy credit history is crucial for many of life’s milestones, from being approved for a home loan to being approved to rent an apartment, to even getting hired for a job. Yet, almost six out of 10 millennials say they’ve been rejected when applying for credit cards, mortgages, car loans and other financial products. While it may feel like the odds are against you in trying to build up your credit history and improve your credit score, with a few financial planning tweaks, you can get there sooner than you think. The SmartCredit system is designed to help you control your future credit score with tools that let you track all your scores with simple charts and an actionable plan to pay down debt and work towards improving your score within 120 days. The SmartCredit System doesn’t just show you what is hurting and helping your credit score, but also reveals specific steps you can take to improve your situation. Learn more about how SmartCredit can help you plan for the future and make smarter financial moves in your 20s. References:

The post The 5 Best Financial Moves You Can Make in Your 20s appeared first on SmartCredit Blog. from https://blog.smartcredit.com/2020/07/02/financial-planning-in-your-20s/ |

About UsWe are a group of fun and creative people building unique and patented technologies for the consumer money, credit & identity space. We started in 2003 with the idea that technology should allow consumers to interact with their banks, creditors and other institutions using a simple button. So, we noodled a lot and built the SmartCredit.com® system to make better users of money & credit. Archives

October 2020

Categories |

RSS Feed

RSS Feed